President Donald Trump has been in the news recently talking about student loan relief due to the coronavirus situation. 2020 has been a stressful year for everyone financially, especially for people with student loans, and many are wondering what the future holds.

The stress of debt is heavy, which is why I created the Student Debt Blueprint for everyone. Covid has definitely made things crazy, but there is some news regarding student loan relief.

President Trump has issued a memorandum regarding student loans, so let’s look at the important information dealing with this situation.

Covid-19 has really thrown a wrench into things, so it’s important to understand the student loan relief that has been issued.

In President Trump’s executive order he announced that federal student loan payments will be frozen until December 31, 2020.

This gives everyone a bit of temporary relief.

The 3 Key Factors on Federal Loans in his Memorandum include:

- 0% Interest Rates

- Frozen Payments

- “Counted” Monthly Payments towards Public Service Loan Forgiveness

Student loan benefits were initially put into place in March when Congress passed the Cares Act, and they were only supposed to last until September.

However, due to the continuing Covid situation, President Trump had these loan benefits extended until the end of the year.

Although unemployment has inevitably risen due to Covid, some people are actually taking advantage of the zero percent interest benefits.

Some people are still working, while others have picked up side hustles in order to pay off their student loans faster.

If you are concerned on what to do, you need to grab the Student Debt Blueprint to help guide you on your debt-free journey.

You will learn the best tactics on how to escape that rotten debt, along with learning how to make more money.

Along with this, people want to know what President Trump plans on doing for student loan forgiveness in general.

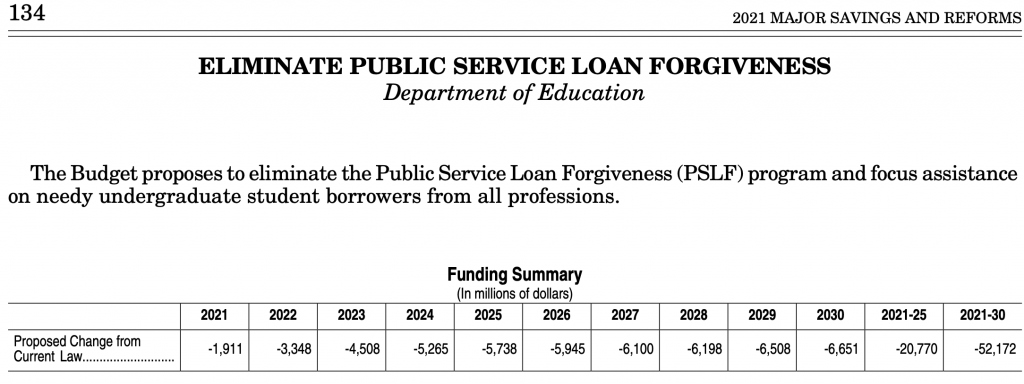

End of the forgiveness program?

The Public Service Loan Forgiveness Program forgives the remaining balance of your student loans after you have made 120 qualifying monthly payments while working a public service job.

This program would most likely be eliminated based on Trump’s proposed budget. This would apply to any future borrowers, so people who are currently part of the program would not be affected.

The United States Secretary of Education, Betsy Devos, and President Trump want to find a medium for both federal taxpayers and student loan borrowers. They make the case that eliminating this program would save the federal government billions of dollars through the avoidance of these student loans.

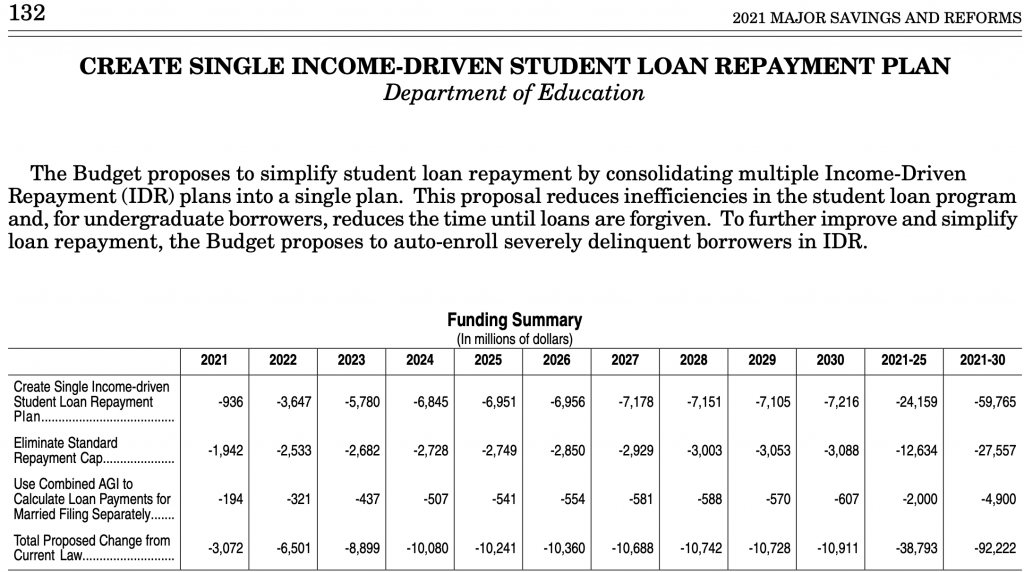

One Repayment Plan

Although President Trump wants to part ways with the PSLF program he actually has a plan to address the student loan forgiveness dilemma. Trump believes that an income-driven repayment plan is the answer to student loan forgiveness.

The income-driven repayment plans currently available include:

- Pay As You Earn (PAYE)

- Income-Based Repayment (IBR)

- Revised Pay As You Earn (REPAYE)

- Income-Contingent Repayment (ICR)

Clearly you can see there are a few options available, however, the President plans to reduce that number to just one.

He thinks that making a concentrated effort towards one single plan is the best solution for borrowers to pay off their student loans faster.

UNDERGRADUATE VS. GRADUATE LOANS

Undergraduate Loans

Under the current income based repayment plan, it takes 20 years of payments until you can seek forgiveness on your undergraduate student loans.

Trump’s plan is to introduce an income based repayment program that allows you to seek forgiveness after 15 years of payments instead of 20.

Essentially, you would be able to get forgiveness 5 years earlier with Trump’s new program. There s obviously going to be important information regarding taxes, so it will be important to read the fine print.

Either way, that is still a long time to be paying off loans.

(Get my Guide if you are sick of Sallie Mae on your back)

Graduate Loans

In addition to undergraduate loans, there are going to be modifications made to the current graduate forgiveness programs.

Under the current income based repayment plan, it takes 25 years of payments until you can seek forgiveness on your graduate student loans.

Trump’s new plan wouldn’t allow graduates to seek income based forgiveness until after 30 years of payments have been completed.

You may be curious as to why the plan is to make it longer. The short answer is because people who have a graduate degree have a higher earning potential than those with an undergraduate degree.

These people have a lower chance of defaulting on their student loans which is why there is going to be more of an emphasis on the undergraduate program.

The future is unpredictable

No matter who gets elected into office this year you should anticipate some changes along the way.

In these challenging times, it is completely normal to be anxious about the future. With that being said, the most important thing to do is focus on what you can control.

When it comes to Congress and the President, there is always going to be back and fourth on the student loan topic.

At the end of the day, no one wants to be in debt. The quickest way to escape the treacherous traps of the financial world is to educate yourself and then put in the work.

If you are still unsure where to start grab the Student Debt Blueprint.

Boss up!

Greetings from Florida! I’m bored at work so I decided to

check out your website on my iphone during lunch break.I really like the knowledge

you present here and can’t wait to tae a look

when I get home. I’m surprised at how fast your blog lopaded

on my cell phone .. I’m not even using WIFI, just 3G .. Anyways,

wonderrful site!

https://writemyessaybest.com/

buy my essay

buy my essay

https://writemyessaybest.com/ https://writemyessaybest.com/